- Subway continues to be one of the cheapest restaurant brands to franchise.

- But declining yearly sales and hundreds of store closures have hurt the company and franchisees.

- Some franchises tell Insider that operators are trying to unload locations at “dirt-cheap” prices.

At the peak of its expansion, Subway was one of the hottest restaurant chains to own as a franchise operator. The chain used middlemen known as development agents to rapidly grow across the US. It became the largest chain in America, leapfrogging over industry giants like McDonald’s and Starbucks.

Many Subway operators have amassed dozens of stores, made possible by historically cheap franchise investment costs.

Initial investment costs are $139,550 to $342,400, according to Subway’s 2020 disclosure document. For comparison, Jimmy John’s requires $313,600 to $556,100 in initial investment costs, and McDonald’s costs are $1.3 million to $2.3 million.

But as the distressed sandwich chain lays off hundreds of corporate staff to cut costs amid rumors of a company sale, franchisees and experts say investing in a Subway outfit comes with big risks these days.

That’s prompting some franchisees to consider selling their stores amid improving foot-traffic patterns as the economy slowly emerges from the devastating effects of the coronavirus pandemic.

“Franchisees, in general, are extremely disgruntled,” one current California franchisee said. He and other franchisees were granted anonymity in order to speak frankly about the situation, and their identities are known to Insider.

This franchisee said some operators were unloading stores “dirt cheap” just to get out of leases or ownership.

Subway pushed back on the conclusion that the company does not offer a return on investment for franchisees. In an emailed response to Insider, a representative said that the company pledged $80 million in 2018 toward helping franchisees refresh the brand.

“This includes money spent on a variety of initiatives, ranging from refresh packages for each U.S. restaurant, grants for remodels and supplying them with new equipment for various programs,” the representative said. “We remain laser-focused on our franchisees’ growth and profitability.”

A Subway franchisee from the Midwest told Insider: “Anybody that wants to buy into any kind of restaurant franchise probably needs to have their head examined. I can’t think of a worse category to really look at. With that said, I think there’s actually some real bargains out there in the Subway world right now.”

The bargains come as Subway, along with the rest of the industry, continues to experience a decline in visits, even as business restrictions lift across the US.

Visits to quick-service sandwich restaurants declined by 10% in the year ending in February compared with the same period a year ago, according to the market-research firm NPD Group.

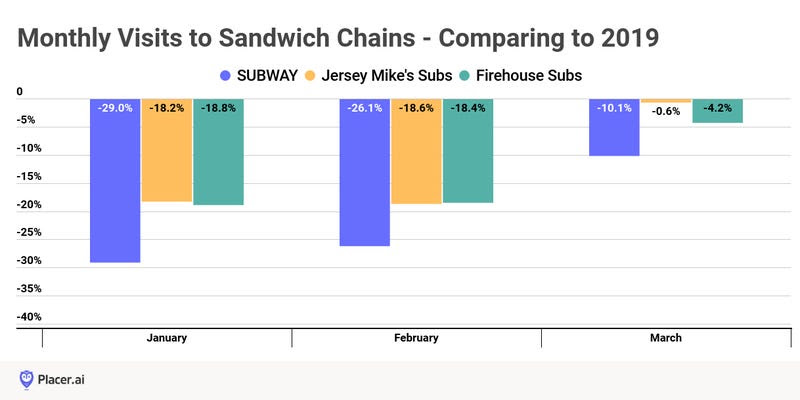

According to Placer.ai, which tracks monthly foot traffic at retail and restaurant chains, Subway traffic declined more than its main rivals over a two-year period. In March, Subway traffic was down 10.1% compared with March 2019, while Jersey Mike’s was down 0.6% and Firehouse Subs was down 4.2%.

Subway’s troubles started long before the pandemic

The 100%-franchised chain has logged declining sales and store counts for years.

Subway’s US sales dropped to $8.3 billion in 2020, down from $10.2 billion in 2019, according to Technomic. The market-research firm’s data indicated 1,796 Subway locations closed in the US last year, with the chain’s store count dropping to 22,005 from 23,801.

For operators, the numbers are more troublesome when compared with yearly sales volumes at rival chains like Firehouse Subs, Jimmy John’s, and Jersey Mike’s.

A Subway restaurant, on average, generates nearly $420,000 in sales annually, according to Nation’s Restaurant News’ “Top 200 Restaurants” report, a highly regarded industry survey. According to NRN’s 2020 report, Subway’s average yearly sales that year were down from $445,400 in 2014 — the year before founder Fred DeLuca died and before the Jared Fogle scandal.

“Sales have gotten so low, lower than they’ve been in a long time,” the California franchisee said. “Inflation keeps going up. And Subway was always on that edge” of profitability, the operator added.

Subway did not return a request for comment.

But the Milford, Connecticut-based company previously told Insider that it strived to “balance what’s best for our guests and our franchise owners as we create compelling offers to drive traffic to Subway restaurants.”

When John Chidsey was named CEO in 2019, the former Burger King executive reached out to high-level operators and “said all the right things,” like being there to help operators make profits, according to a veteran franchisee.

But he has since distanced himself from communicating with franchisees, that franchisee said.

Now frustrated operators want out, the California franchise said.

Five years ago, Subway stores could be worth $300,000 to $400,000, the California operator said. If a franchisee could sell their stores for $100,000 each in 2021, they would be considered lucky, the California franchisee added.

Subway is struggling to keep up with rivals

Subway franchisees say they are struggling to stay afloat as competitors like Firehouse Subs and Jimmy John’s raise their game with menu innovation and better delivery operations. The rival chain Jersey Mike’s gave its franchises $150 million to help finance store remodeling during the pandemic.

By contrast, Subway franchises continue to battle corporate over store hours and foot-long deals.

In June, some Subway franchisees filed complaints with the Federal Trade Commission after the chain rolled out a “$5 footlongs when you buy two” deal, Restaurant Business reported. In the fall, Subway also began strictly enforcing the number of hours a week stores were expected to be open, which infuriating franchisees, the New York Post reported. Until then, the company had allowed flexible work hours and deferred royalties during the pandemic, the Post said.

More recently, sources told Insider that Subway axed a rebate corporate would give franchises to cover extra third-party delivery costs tied to tablets used to field delivery orders. In a memo seen by Insider, Subway told franchisees the company had always intended to “sunset this program once POS integration was completed.”

Subway told Insider the company “supported our franchisees by temporarily offsetting some the program’s initial costs” during the rollout of third-party delivery in 2018.

“As with everything, we take a holistic approach to all factors that touch our franchisees’ businesses with the goal of increasing profitability, including negotiating highly competitive third-party delivery rates,” the company said in a statement sent to Insider. “We continue to invest in programs to help our franchisees grow their business.”

The Subway franchisee from the Midwest said the biggest pain point for franchisees over the past several years had been the company’s deep reliance on discounting, which he said accounted for 60 to 70% of the marketing strategy in 2015.

“Our margins just kept eroding,” the Midwest franchisee said. “When the guest counts weren’t going up, and sales weren’t going up, they just piled on more and more discounts. So 2015, ’16, and ’17 were absolutely the worst years I’ve ever had in this business.”

Over the years, Subway operators have been hooked into buying franchises because of the lower startup costs when compared with rival chains, according to 2020 franchise-disclosure documents reviewed by Insider.

When you look at the startup cost and take in the average yearly sales volumes, industry experts and franchisees said now was not the time to invest in Subway, which also charges higher royalty fees than their competitors.

Subway takes an 8% cut of total gross sales, according to its franchise-disclosure statement. Royalties for Firehouse Subs franchisees range from 3 to 6%. And Jimmy John’s takes a 6% cut of gross sales, according to the documents.

Ultimately, Subway franchises are getting hit with a larger royalty fee on declining sales, and they are likely paying the same rent as rival sub shops like Firehouse Subs, the franchise developer Dan Rowe told Insider.

“It’s a terrible franchise now with these volumes,” Rowe, the founder and CEO of Fransmart, said.

Rowe, who helped develop Five Guys coast-to-coast through franchising, said “the point of franchising is to get wealthy, financially independent, and live a great life.”

That’s not happening at Subway, he said, where many franchisees are risking their life savings to invest in a franchise system that is not a good investment.

“It’s quite sad for the franchisees,” he said. “A job is actually better because you aren’t risking your life savings, and you can always quickly quit a job. If you don’t like your Subway, you are stuck until you can sell it, and even then the landlord may keep you on the lease.”

Pacific Management Consulting Group’s John Gordon told Insider that “this is not the time, under any circumstance” to buy a Subway location.

“Find any kind of other brand, particularly one with the drive-thru,” Gordon said. “You need a drive-thru in this post-COVID environment.”

Still, the restaurant consultant Gary Stibel said Subway could still be a very good investment “as long as you’ve got a good location” that is not near rivals, which include convenience stores and premium sandwich shops like Jersey Mike’s.

Stibel, the founder and CEO of the New England Consulting Group, said Subway’s “value proposition has aged but it hasn’t staled.”

If a new owner or current leadership revives the brand, “there is the potential for Subway to come back stronger than it ever was before,” Stibel said.