Compared to years and decades ago, restaurant managers at all levels have so much more information. When I started in 1978, it was about French fry yields, meat variances, and labor hours versus chart. Those key performance indicators (KPIs) are still important but now there are real time guest ratings and guest flow indicators to manage.

I’m working a corporate transformation project for an international multibrand franchisee with several US brands. They are very sophisticated and invested greatly in management systems. One of the findings we realized is the data itself seen every month needed to be examined from a 30,000 foot view; one month of results was not a call to action but interesting, rather best seen as a part of the puzzle to be seen from above. The lesson: take your time but not too much time to see the trend.

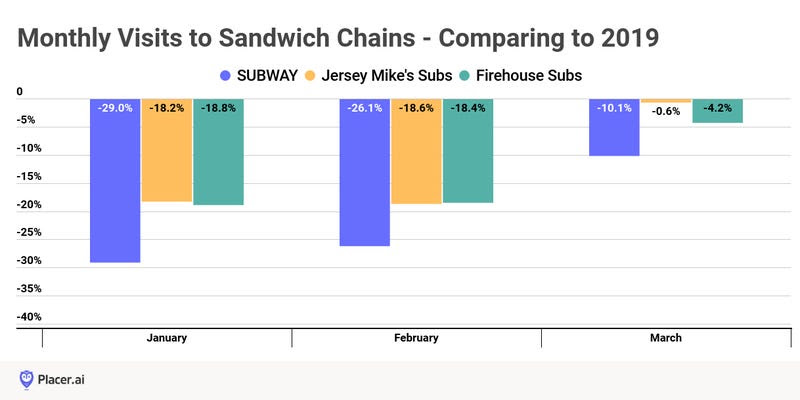

A Promising View From Above

We are amid Quarter One restaurant earnings and the results have been spectacular when viewed against 2020. Of course, 2020 is the worst base in the world to compare to as that was the Pandemic year. Most but not all companies and analysts have shifted their focus to discussion against 2019 as the base. Facteus, the consumer spending reporter based on credit card sampling, shows healthy weekly full service and quick service spending gains versus 2019 through May 4 via their FIRST system. To be sure, the full-service segment did not hit positive until March when the Biden stimulus funds began to flow. On Friday, May 7, the number of US passengers clearing TSA gates was 1.7 million, a post Pandemic record, but still, a way to go from the 2.4 million average pre March 2020 and in 2019. [1] Coresight Research reported that via their sampling, more consumers dined at restaurants in late April to May and are resuming general social activities.[2]

Every time that cash has been injected into the economy, restaurant sales have taken off. So it is logical to assume that there will wear off as the funds are spent down. The good news is the stimulus raised restaurant demand into our historical peak months of May-August. While vaccine progress continues, it is slower than we might hope. I am watching movie and sports events attendance as well as summer travel as factors to offset the wear off of the stimulus effect. We also need resumption of meetings and conventions, which there are promising signs this fall. Watch this space for future developments.

IPOs, and SPACs in the Restaurant Space: Do Your Due Diligence

Very good signs point to new IPOs coming: Torchy’s and Dutch Bros. are making all the right signs and moves. Torchy’s Taco’s lead by veteran CEO G.J. Hart presented at the 2019 ICR Exchange and its momentum (and good food) then was clear. Dutch Bros. is a small box coffee DT chain in Oregon and Northern CA featuring specialty coffee and is a real draw here. What was more surprising was that Krispy Kreme announced that it had filed private documents with the SEC to go public. It was surprising to me only that JAB Holding, the Luxemburg family holding fund had such strong results with Krispy, especially international results, since 2015.[3] One very strong motivation: the stock market has soared in most sectors for all kinds of reasons. Investors and prospective companies seek returns.

There is also a literal boatload of restaurant SPACS present, 8 by the count of Jonathan Maze in March.[4] A SPAC is a specialty purpose acquisition company, which raises money and has two years to make an acquisition. Often, restaurant insiders are part of the board and serve as “rainmakers”. SPACS have been used for years, they offer quicker access to the stock market listing. Burger King was a SPAC listing in 2012. However, due diligence on smaller companies is recommended. For example, the highly promoted better burger BurgerFi went through its SPAC process but then was unable to publish its first annual audited financial statements. As a result, it recently received the routine warning from NASDAQ that it was out of compliance with the Exchange’s rules and that it must comply.[5]

For that matter, most investors prefer the traditional IPO process, with a S-1 disclosure document, roadshows, and known investment banks. I can’t stress the importance of reviewing baseline financial statements (income statement, balance sheet, and sources and uses of cash) and outyear projections critically, comparing to as many different scenarios as possible.

Chicken Sandwich Product Development Note: New News Please

Early in my corporate staff career (finance), I got the opportunity to work with both supply chain and concept and product development routinely. As the chicken sandwich wars have covered the globe, imagine my amazement that every chicken sandwich is essentially the same with the same flavor profile. This is just beyond belief. I would have thought there would have been some variability, some chain claiming some unique flavor profile. Apparently not. Of course, I understand the need for QSR simplicity and uniformity coming from that segment initially. Hopefully, some QSR brand can pull off a marketing and product development coup by adding sauces/flavors/seasonings.

About the author: John A. Gordon is a long time restaurant analyst and management consultant. He specializes in operations, financial management and strategic assessments and reviews for clients, including investor due diligence and litigation support. He is a master analyst of financial forensics (MAFF) and can be reached at jgordon@pacificmanagementconsultinggroup.com, office 858 874-6626.

[1] See https://www.tsa.gov/coronavirus/passenger-throughput

[2] Coresight Research, May 10, 2021.

[3] Restaurant Business Online, The Bottom Line, May 5 2021

[4] Restaurant Business Online, Here Are All the Restaurant SPACS Right Now, March 17 2021.

[5] Nation’s Restaurant News, NASDAQ warns BurgerFi…, April 20, 2021.